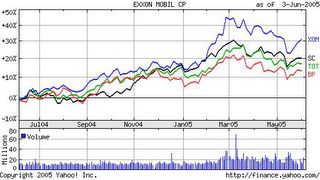

Lately, I’ve been doing a bit of researching Big Oil. At first glance, it looks like ExxonMobil –the biggest private energy firm—is doing best, by far. Over the last 12 months its stock has been the top performer in this group and it enjoys the highest valuation by any measure. .

.

Seeing this, I was sure its operating figures must be much better than those of other (such as BP, Shell and Total). But digging deeper, this proved to be very, very false: Exxon has some of the worst figures in the industry.

For instance, take production. According to my calculations, its total oil & gas output has fallen over the last four years (by 1.5%), while BP raised it by 23% and Total by 22%. Reserves, refining and product sales point the same way.

Yes, it’s generating tons of cash for shareholders (nearly 16 billion between dividends and repurchases last year). But this also reflects the fact that it invests much less than its competitors: Exxon’s capital expenditures only took up 30% of its operating cash flow (net income + depreciation), while the other firms invest over 50%.

So, we’re talking about a firm that is basically not growing in real terms, that is probably shortchanging its future by underinvesting and whose stock is pretty expensive.

This makes me wonder whether I’m the only one missing something or most everyone else is in the dark. Well, for what its worth, I believe Total is the best choice in this group, followed by BP.

Monday, June 06, 2005

Best bet among the oil majors?

Subscribe to:

Comment Feed (RSS)

|